Payment service providers (PSPs) from London landed seven funding rounds of over $20 million in the first half of 2021 -- considerably more than any other global city -- new deals data from 451 Research reveals.

The data comes as venture funding for PSP companies reached $5.56 billion in the first half globally, as technology continues to disrupt and throw up opportunities in a rapidly evolving sector.

(From real-time payments to SWIFT gpi, blockchain and digital currencies, entrepreneurs, investors and financial services companies are looking to shake up the "slow, expensive and opaque" world of cross-border payments in particular; riddled as it is by compliance costs and often complex back-end arrangements.)

Payment service providers: "Start with a large fortune..."

Jordan McKee, author of the report and principal analyst for digital payments at S&P Global Market Intelligence, noted: “Our research suggests an optimistic growth outlook for the payment service providers segment, buoyed by merchants that have a heightened need for modern payments infrastructure coming out of the pandemic."

He added: "The fastest way to make a small fortune in payments is to start with a large fortune.

“That's the current mantra in the payment service provider segment, where nine-figure rounds have become commonplace for driving growth and product diversification. More commerce shifting online has meant accelerated transaction volume and customer growth for market participants, while also helping to bolster demand for their ancillary services in areas such as fraud prevention."

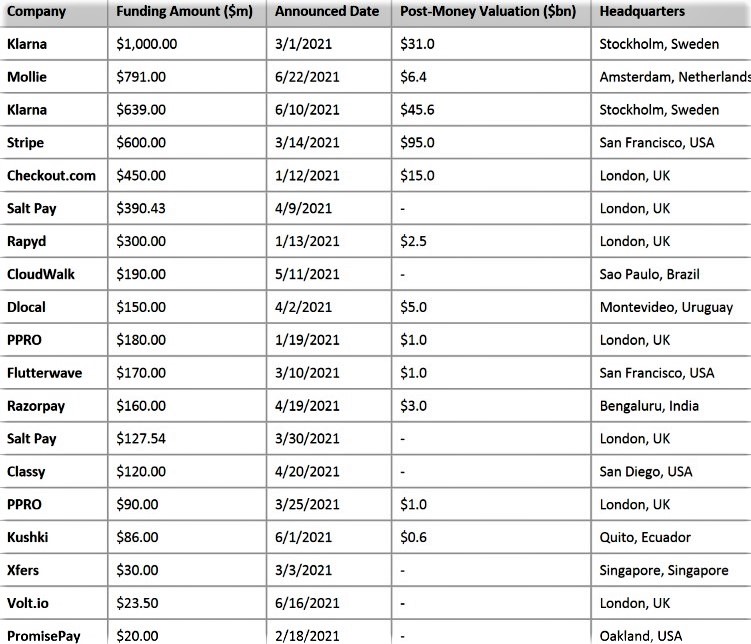

Checkout.com, PPRO, Rapyd, and Salt Pay, Volt.io from London all saw substantial funding rounds in H1. As did Stripe (Dublin/San Francisco), Klarna (Sweden) and Mollie (Netherlands).

McKee said: "Europe has emerged as a hotbed for PSP activity and funding. More than 70% of the $5.56bn raised by PSPs in the first half went to those headquartered in Europe. There are several factors that make Europe a particularly intriguing market for PSPs. The regulatory landscape (e.g., PSD2), prevalence of local payments methods and overall fragmentation of the market provide multiple avenues for competitive differentiation."

Outside of Europe Nium, a Singapore-based global B2B payments platform, today (July 27) announced it has raised a $200+ million Series D round led by Riverwood Capital, as the pronounced investor interest in payments companies continues. Nium will use the Series D funds to expand its technical infrastructure and add new embedded fintech services. Through a single API, Nium provides access to the world’s payment infrastructure, including technologies for pay-outs, pay-ins, card issuance, and banking-as-a-service.

As 451 Research notes, however: "While legacy processors have historically led much of M&A in the payments industry, deep-pocketed payment service provider startups are becoming increasingly active. Stripe, for instance, made two acquisitions in the first half of the year, nabbing TaxJar (tax software) in April and Bouncer Technologies (fraud prevention) in May. Checkout.com acquired Estonian software development vendor Icefire in June, while Rapyd paid $100m on July 1 for Valitor, to deepen its merchant acquiring capabilities.

"Klarna has looked to deepen its commerce proposition through M&A this year, with acquisitions of Toplooks (content) in March and Hero (social shopping app) in July. SaltPay, on the other hand, has come together almost entirely through an M&A rollup strategy, with acquisitions of Paymentology (issuer processor), Tutuka (issuer processor) and Storyous (point-of-sale software) this year, and Borgun (PSP) in 2020. Looking ahead, we anticipate that many of the PSPs that have amassed significant capital in H1 2021 will begin deploying more of it in the form of M&A."

The market activity comes amid shifts in both retail and wholesale payments.

As the Bank of International Settlements (BIS) noted in 2020: "Wholesale [payments] systems are opening up access to non-banks, extending operating hours and improving the interoperability of systems. Fast or instant retail payment systems have been or are being developed in many jurisdictions. However, shortcomings in access and cross-border payments remain. Access issues can be addressed through targeted interventions in individual jurisdictions. Quantification of the extent and relative importance of the various drivers facilitates such interventions. Fintech is also likely to improve universal access to and frequent usage of transaction accounts."

{kind=link}