Seeking a new gas boiler for The Stack’s bracingly cold HQ, we were told this week that the model sought was unavailable. Why? A global semiconductor shortage that has caused shortages in unexpected industries, quoth the gasman. Boilers increasingly use wireless control units that, like most things digital, require a small chip as their brain. Without them, many are now great dumb chunks of metal unable to warm so much as a thimble of water. They’re not alone in having lost their digital marbles: the issue has hit suppliers of air conditioners, cars and of course, PCs and servers. So will this chip shortage in 2022 be as pronounced as it was in 2021?

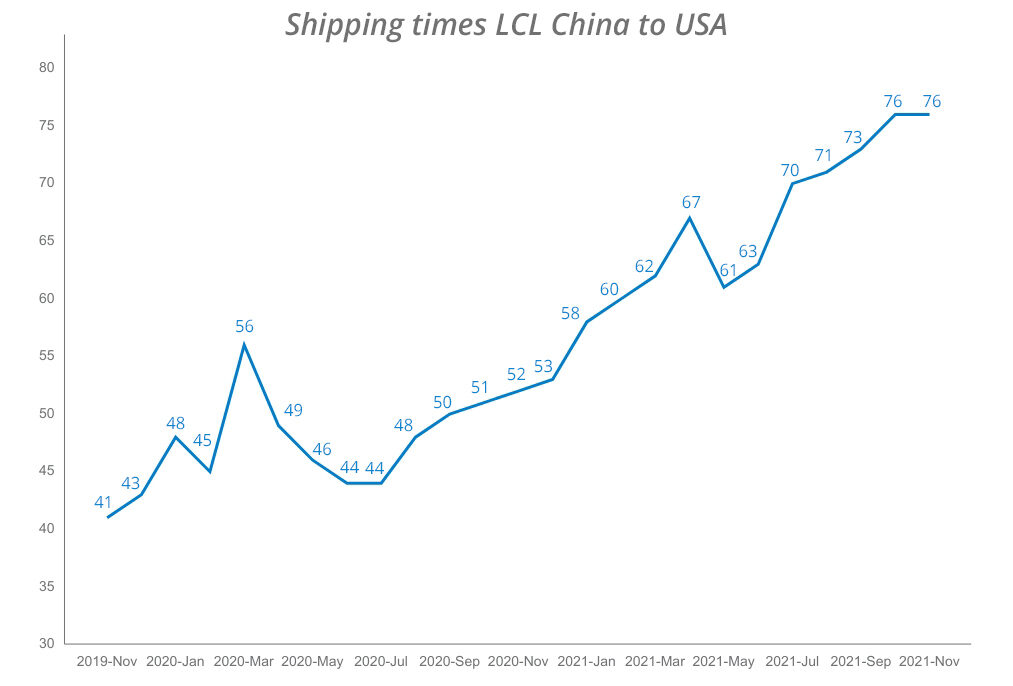

Covid shutting down factories, labour shortages at ports and airports and hugely volatile freight prices are certainly not helping with the recovery. (In 2016 ocean freight rates were so low that they triggered the bankruptcy filing of ocean carrier Hanjin. How things have changed: the cost to ship a 40’ container from Asia to the US West coast has soared from $1,300 in August 2021 to over $18,000 in August 2021; broadly, trans-Pacific ocean freight rates have spiked to 9X the pre-pandemic norm, data from specialist Freightos shows.)

So, you ask again, will the chip shortage in 2022 be as bad as it was in 2021? The answer, it appears, is “maybe”. (Per the sagacious words of Yogi Berra, “it’s tough making predictions, particularly about the future”.)

The great chip shortage in 2022: Plus ça change, plus c'est la même chose?

This week Deloitte predicted that chips will remain in short supply next year, and some component lead times will stretch into 2023. That’s despite the multinational consultancy also predicting that VC firms globally will invest more than $6 billion in semiconductor startups in 2022. (The bottleneck isn’t in design, but the bottle-necked and capex-intensive world of semiconductor fabrication; the industry has huge barriers to entry…)

The issue stretches well beyond semiconductors themselves. As Intel CEO Pat Gelsinger noted on the company’s last earnings call: “Things like ethernet controllers and power supply devices are holding us back from achieving... trust me, we would be shipping a lot more units, right, if we weren't constrained by the supply chain of these other components in the industry. Our customers, both cloud customers and OEMs, very strong backlogs that they're pressing us aggressively to satisfy, but we’re really limited by these ‘match sets’”.

AMD CEO Lisa Su echoed the point, on November 30 telling investors at a Credit Suisse event that "it's every aspect of the supply chain, right? It's wafers, it's back-end capacity, it's substrates, it's logistics, all of that stuff coming together... [but] I would say the entire semiconductor industry has made progress. We also have to recognize that the demand in 2021 is so much higher than any of us thought four quarters ago."

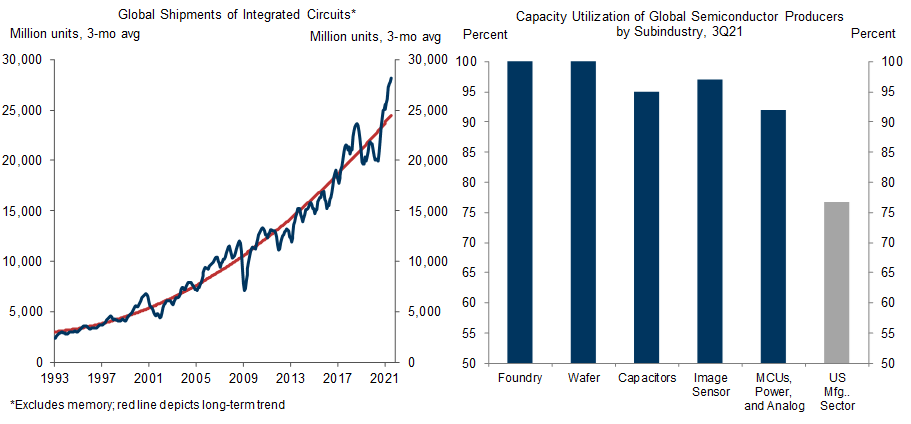

And as Goldman Sachs analysts recently noted, outside of Southeast Asian plant shutdowns, both semiconductor output and capacity utilisation at fabs have “returned to quite elevated levels…”

The ongoing issue, in short, appears to be the high technology icing on top of a monstrous supply chain cake – thanks again, Covid. And demand is rampant. As Goldman put it: “Demand for consumer electronics, business tech, and other semiconductor-intensive products has remained elevated—both globally and in the US. Nor do we expect the increased digitization of society and consumer preferences to reverse post-pandemic: our equity analysts forecast demand for semiconductor-intensive consumer goods to remain strong in 2022 (smartphones +4% after +12% in 2021, autos +5% after +6%, PCs -12% after +28% in 2020 and 2021).

Show me the money!

In the US, CEOs from almost every affected vertical are lobbying hard for funding to boost production.

Congress in January enacted the CHIPS for America Act as part of the FY 2021 National Defense Authorization Act (NDAA) – a law that authorises incentives for domestic semiconductor manufacturing and investments in chip research. Funding for these provisions, however, remains held up, even as industry frustration grows.

And on December 1, 2021, 59 CEOs and senior executives from a range of industries urged “prompt action” on funding, to “include an investment tax credit for both design and manufacturing” and other funding for semiconductor research, design, and manufacturing in the US, “strengthening the U.S. economy, national security, supply chain resilience, and increasing the supply of chips so important to our entire economy.”

(On the national security front, concerns at the fact that, as of 2020, 81% of semiconductor contract manufacturing was based in Taiwan or South Korea continue to grow among geopolitics watchers.)

Apple’s Tim Cook, Google’s Sundar Pichai, Ford’s James D Farley, GM’s Mary T. Barra, and IBM’s Arvind Krishna (as well as the leaders of most semiconductor companies), were among those telling US political leaders in a December 1 letter that “semiconductors are essential to virtually all sectors of the economy – including aerospace, automobiles, communications, clean energy, information technology, and medical devices. Unfortunately, demand for these critical components has outstripped supply, creating a global chip shortage and resulting in lost growth and jobs in the economy. The shortage has exposed vulnerabilities in the semiconductor supply chain and highlighted the need for increased domestic manufacturing capacity.”

They also left our offices colder than we’d like. Something has to give.

Supply chain dysfunction needs some strategic thinking

In such a capex-intensive industry with such long lead times, the potential for such feast-then-famine cycles appears someone what baked in. As Deloitte noted this week, “the world’s three largest semiconductor manufacturers announced cumulative annual capital expenditures of more than US$60 billion for 2021 and will likely spend even more in 2022”. With demand (as Goldman Sachs noted) rampant, there’s a business case for it and supply-demand may yet balance themselves. But not if broader supply chains remain broken.

(Detailing the company’s own investment plans. semiconductor maker Texas Instruments’s Head of Investor Relations Dave Pahl recently told investors that “while there is a growing recognition that the near-term supply demand imbalance will end at some point, the secular growth of semiconductor content per system will continue to grow and this requires a robust manufacturing capacity roadmap for 2025 and beyond.”)

The outlook for the pandemic continues to be another “known unknown”. As John Manners-Bell, director of the Foundation for Future Supply Chain noted on November 30 with regard to government responses to the latest viral mutation: “The Omicron variant isn’t likely to affect underlying demand – [it] may even increase it as loose fiscal policy extended well into 2022. Problem is the response by governments to each new variant will create further supply chain volatility extending present crisis. If this is the ‘new normal’ then we will see Asian manufacturers shut down regularly; ports and airports affected by labour shortages; ships queuing one month and sailings blanked the next; bellyhold capacity rise and fall depending on passenger bans, Western ports and warehouses overwhelmed and continued driver shortages at key times etc. The result?

“Higher inventory, higher transport costs, the move away from JIT (just-in-time), less consumer choice, higher prices i.e. supply chain dysfunction. Whilst this may be acceptable in the short term, the fall out will be increasingly severe - first by SMEs who are feeling the pain of shipping rates and disrupted supply the most; then by larger shippers, [as well as the] indirect consequences of Covid such as industrial action looming at ports. So what’s the solution? Reshoring and shorter, more regional supply chains will help (but unrealistic in material terms). Move away from huge container ships and the use of a few consolidated gateway ports to more agile maritime operations. Develop an air cargo sector independent of passengers; increased automation of ports and warehouses; focus on quality of trucking sector not price. Digitalisation of logistics. Plus more investment in transport infrastructure. In many respects Covid has laid bare the weaknesses of the supply chain and logistics sector. Short term fixes are few and far between so our industry must plan not for a post-pandemic world but to create models which can adapt and thrive in an environment of constant volatility.”

{kind=link}